Internal rate of return (IRR)

The internal rate of return (IRR) is the return on an investment. That is, it is the percentage profit or loss that an investment will make for the amounts that have not been withdrawn from the project.

A measure used in the evaluation of investment projects to test the viability of an investment. It allows investments to be compared with each other. The higher the IRR, the better the investment.

It is closely related to the net present value (NPV). In fact, the IRR is also defined as the value of the discount rate that makes the NPV equal to zero, for a given investment project.

The internal rate of return (IRR) gives a relative measure of profitability, i.e. it will be expressed as a percentage. The main problem lies in its calculation, since the number of periods will determine the order of the equation to be solved. To solve this problem, various approximations can be used, such as a financial calculator or a computer programme.

When assessing the viability of an investment project, it is important to take into account the discount rate of the project. If the discount rate is higher than the IRR, the project is not viable, because it costs more to finance the project than the long-term return on the investment, after discounting the future payments to their present value. For example, if the IRR is 3%, but the discount rate is 5%, the project is not viable.

How is IRR calculated?

It can also be defined based on its calculation, the IRR is the discount rate that equals, at the initial moment, the future flow of collections with that of payments, generating an NPV equal to zero:

- Ft are the money flows in each period t

- I0 is the investment made at the initial moment ( t = 0 ).

- n is the number of time periods

Project selection criteria according to internal rate of return

The selection criteria will be as follows, where «k» is the discounted cash flow rate chosen for the NPV calculation:

- If IRR > k, the investment project will be accepted. In this case, the internal rate of return we obtain is higher than the minimum rate of return required for the investment.

- If IRR = k, we would be in a situation similar to that which occurred when NPV was equal to zero. In this situation, the investment can be carried out if it improves the company’s competitive position and there are no more favourable alternatives.

- If IRR < k, the project should be rejected. The minimum return on investment required is not achieved.

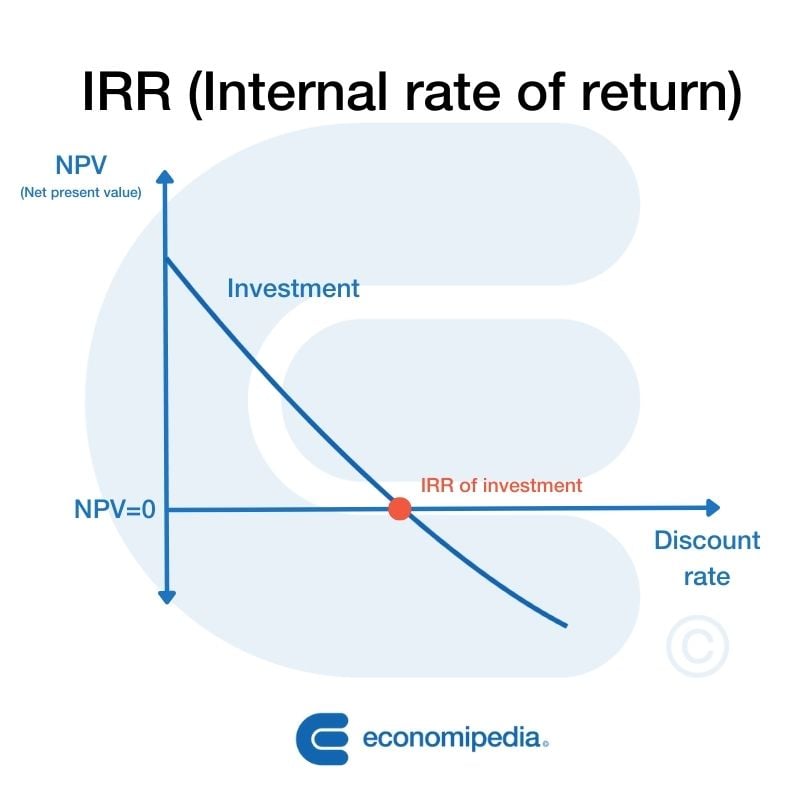

Graphical representation of IRR

As mentioned above, the Internal Rate of Return is the point at which the NPV is zero. So if we draw the NPV of an investment on a graph on the ordinate axis and a discount rate (profitability) on the abscissa axis, the investment will be a downward curve. The IRR will be the point where that investment crosses the abscissa axis, which is the place where the NPV is zero:

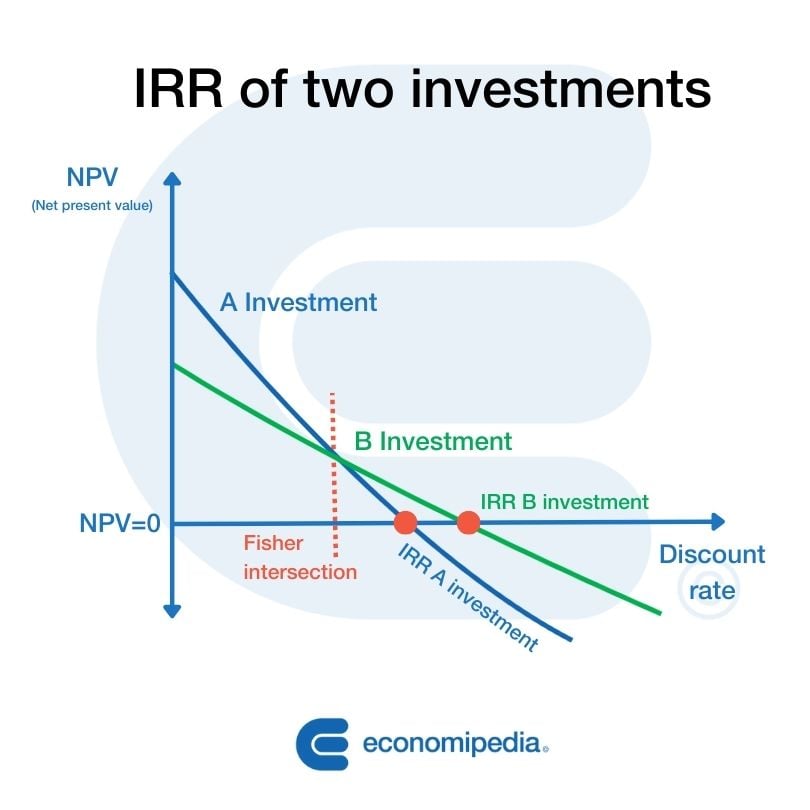

If we draw the IRR of two investments, we can see the difference between the calculation of NPV and IRR. The point where they intersect is known as the Fisher intersection.

Disadvantages of the Internal Rate of Return

It is very useful for evaluating investment projects as it tells us the profitability of such a project, however it has some drawbacks:

- Intermediate cash flow reinvestment assumption: assumes that positive net cash flows are reinvested at r and that negative net cash flows are financed at r.

- The inconsistency of IRR: it does not guarantee to assign a profitability to all investment projects and there are mathematical solutions (results) that do not make economic sense:

- Projects with several real and positive r’s.

- Projects with no economic sense.

Example of IRR

Suppose we are offered an investment project in which we have to invest 5,000 dolars and we are promised that after this investment we will receive 2,000 dolars in the first year and 4,000 dolars in the second year.

Therefore the cash flows would be -5000/2000/4000

To calculate the IRR we must first equal the NPV to zero (equating the total cash flows to zero):

When we have three cash flows (the initial one and two more) as in this case we have a second degree equation:

-5000(1+r)^2 + 2000(1+r) + 4000 = 0.

The «r» is the unknown to be solved. That is, the IRR. We can solve this equation and it turns out that r is equal to 0.12, i.e. a profitability or internal rate of return of 12%.

When we have only three cash flows as in the first example, the calculation is relatively simple, but as we add more components, the calculation becomes more complicated and we will probably need computer tools such as excel or financial calculators to solve it.

Another example of IRR…

Let’s look at a case with 5 cash flows: Suppose we are offered an investment project in which we have to invest 5,000 dolars and we are promised that after this investment we will receive 1,000 dolars in the first year, 2,000 dolars in the second year, 1,500 dolars in the third year and 3,000 dolars in the fourth year.

So the cash flows would be -5000/1000/2000/1500/3000

To calculate the IRR we must first equal the NPV to zero (equating the total cash flows to zero):

In this case, using a financial calculator it tells us that the IRR is 16%. As we can see in the NPV example, if we assume that the IRR is 3% the NPV will be 1894.24 dolars.

The excel formula for calculating the IRR is called «tir». If we put in different consecutive cells the cash flows and in a separate cell we incorporate the whole range it will give us the result of the IRR.

You may also be interested in the comparison between NPV and IRR.

Autores

Publicado por Andrés Sevilla Arias (CFA) el 13 marzo 2023.

Revisado por última vez el 23 marzo 2023.

Cómo citar este artículo

Sevilla Arias, A. (2023). Internal rate of return (IRR). Economipedia. https://economipedia.com/definiciones/internal-rate-of-return-irr.html

Sobre Economipedia

Este artículo forma parte de la enciclopedia de Economipedia, una plataforma de educación financiera que ayuda a millones de personas a entender la economía, aprender a invertir y mejorar sus finanzas personales. Fundada en 2012 por Andrés Sevilla Arias y desarrollada por más de 50 economistas y asesores financieros.

Todavía no hay comentarios

Hay 2 tipos de personas: las que leen y se van…y las que dejan huella 👇